A Better Home Loan starts with

a Better Interest Rate

Quick Quote. NO SSN, NO Credit Check, NO Hassle, Start Here to Compare Rates >>>>>>

Stephanie Medellin

Loan Officer

We offer low mortgage rates along with a convenient online loan application process supported by a team of experienced loan officers.

Phone: (714) 603-9383

NMLS#: 876196

License: CA

Spoken Language: English

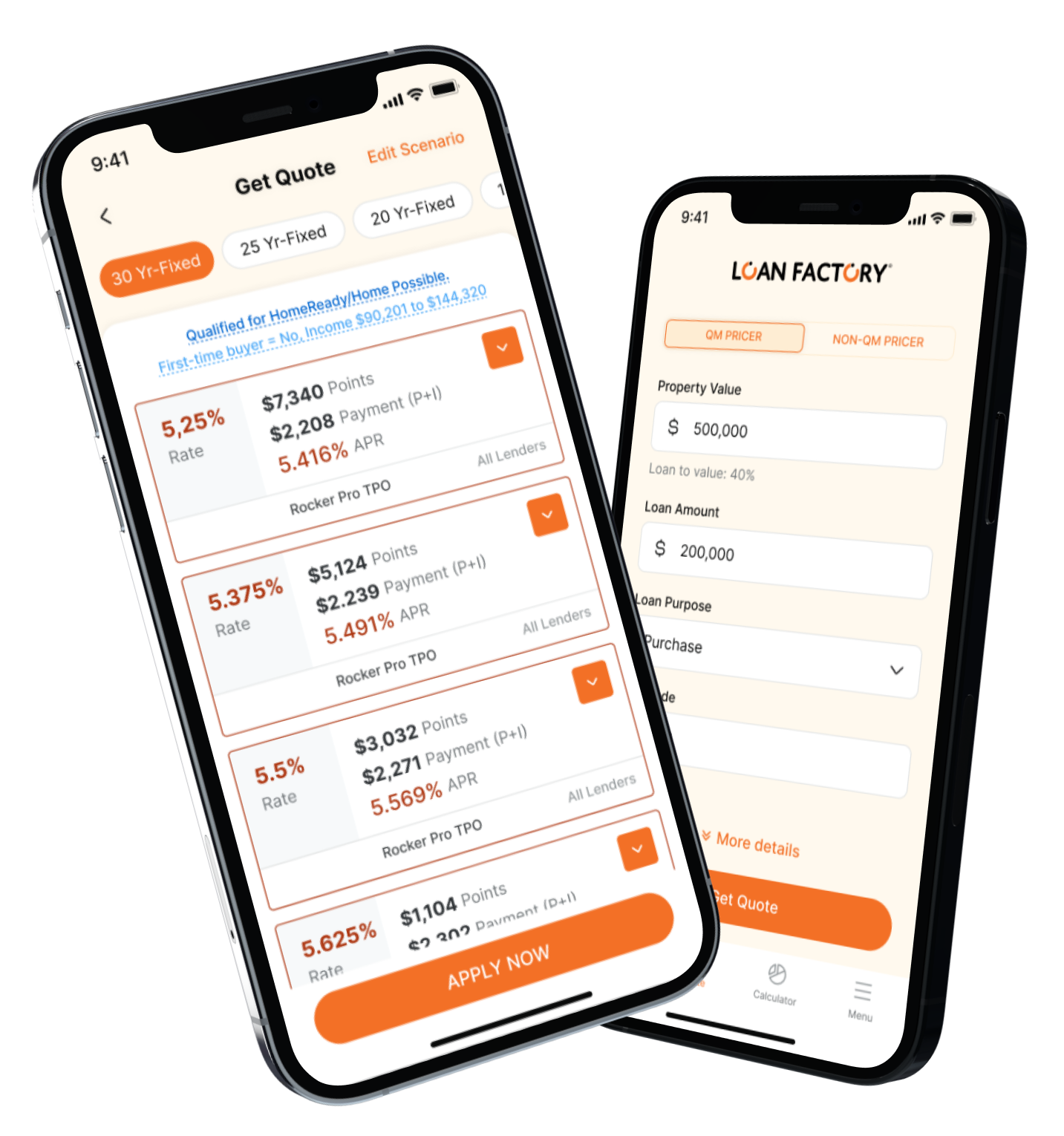

Mortgage Rates

Why are our rates so low?

- 1. WE SHOP RATES FOR EVERY LOAN: We compare rates from 240 lenders in real-time for you.

- 2. WE NEGOTIATE FOR YOU: Loan Factory is the fastest-growing Mortgage Broker in the United States. Because we have closed so many loans, we can negotiate and obtain ridiculously low rates from lenders.

- 3. WE LOWER OUR PROFIT: Our profit per loan is much lower than that of our competitors. We aim to earn your business and your referrals.

OUR ACCOMPLISHMENTS

240+

Number of Lenders

11217+

1750+

Ready to get started?

We are here to help you find a great deal.

Services We Offer

Home Purchase

Are you a first-time home buyer? We will guide you through the whole process from pre-approval to closing with our convenient and easy online application.

Refinance to a Lower Rate

Need to refinance to get a better rate or different terms? Refinance to put yourself in a better financial position. Rates are updated in real time from lenders so you can capitalize on a great opportunity.

Refinance to Get Cash Out

A cash-out refinance is one of several ways to turn your home's equity into cash. We will help you with your financial plan.

Rudy provided a great buying experience for me in purchasing a home in Monterey Park, CA. He knew the area well, provided excellent guidance, responded quickly when I had questions, and also help me negotiate a highly competitive house that was hot on the market. Thanks Rudy!

Aileen was a pleasure to work with, she helped us to buy a home which we were waiting for a long time. She goes above and beyond to get things done on time. Very prompt in follow ups, responding to emails and text messages. I strongly recommend Aileen if you are buying a house, you can rely on.

Michael is a professional and a gentleman. He was always on time; always prepared; always willing to go the extra mile. He answered all of our questions and provided details and explanations when we were puzzled. He was never flustered, never in a hurry, and never angry. Michael was a pleasure to work with. We are immensely satisfied with Michael's service.

Why Clients Choose to Work With Us

Independent Advice

We are committed to always giving you independent advice regarding real estate and mortgage options.

Customers Come First

We make less per loan than competitors and pass the extra savings to borrowers.

Low Available Rates

See current daily rates customized to your loan scenario on our real-time pricing engine.

Fast, Convenient Service

We are just one call away when you have questions.

Fast funding,

easy application.

Get your loan today!

Quick Loans, Anytime, Anywhere!